Monitoring the amount of wealth hidden by individuals in international financial centres

Report by ECORYS 2021

Summary

Tørsløv, Wier and Zucman estimate the scale of profit shifting to low-tax jurisdictions by multinational enterprises (MNEs) based on macroeconomic data, namely Foreign Affiliates Statistics (FATS) and bilateral balances of payments. The data reveal that MNEs’ affiliates in tax havens are much more profitable than local firms. This cannot be explained by the fact that MNEs are in general more profitable, since MNEs in non-haven countries are less profitable than local firms. In addition, the average profitability of local firms is similar in tax havens and non-havens. This suggests that economic activity is not generally more profitable in tax havens but that the disproportionate profits of MNE in tax havens can be explained by profit shifting.

Based on the observed discrepancy of profitability, the authors estimate that in 2015, 616 billions USD out of 1.7 trillion USD of multinational profits (or 36%) were artificially shifted to tax havens. This result is consistent with the abnormal level of cross-border payments conducive of profit shifting received by tax havens. Such high-risk cross-border transactions include royalty payments, intra-group interest receipts and certain services (financial, headquarter and communication technology etc.). Bilateral data on the origin of these high-risk payments allows the authors to propose a geographical distribution of shifted profits and associated corporate income tax revenue losses. For example, if 30% of high-risk payments received by the Cayman Islands come from the US, the US is allocated 30% of profits found to be shifted to this tax haven.

The results identify EU countries as the most severely harmed, with about 35% of profits shifted globally. Besides, relatively to the size of their economy, tax havens generate much more fiscal revenue than higher-tax countries, despite low statutory and effective corporate income tax rates.

Key results

Policy implications

Data

The authors use different macroeconomic datasets including:

Go to the original article

The original paper, data sources, and computations can be downloaded from the missingprofits.org website. [pdf]

Monitoring the amount of wealth hidden by individuals in international financial centres

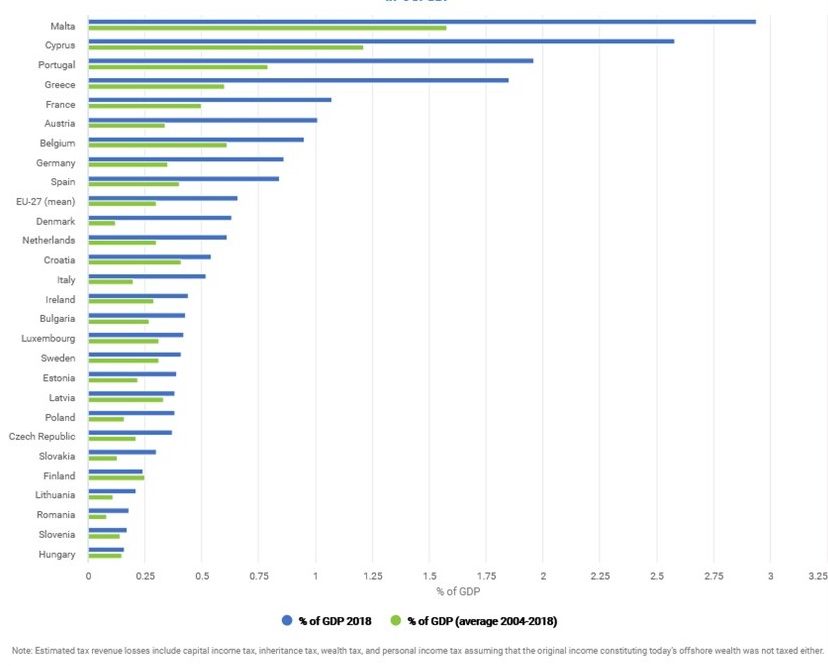

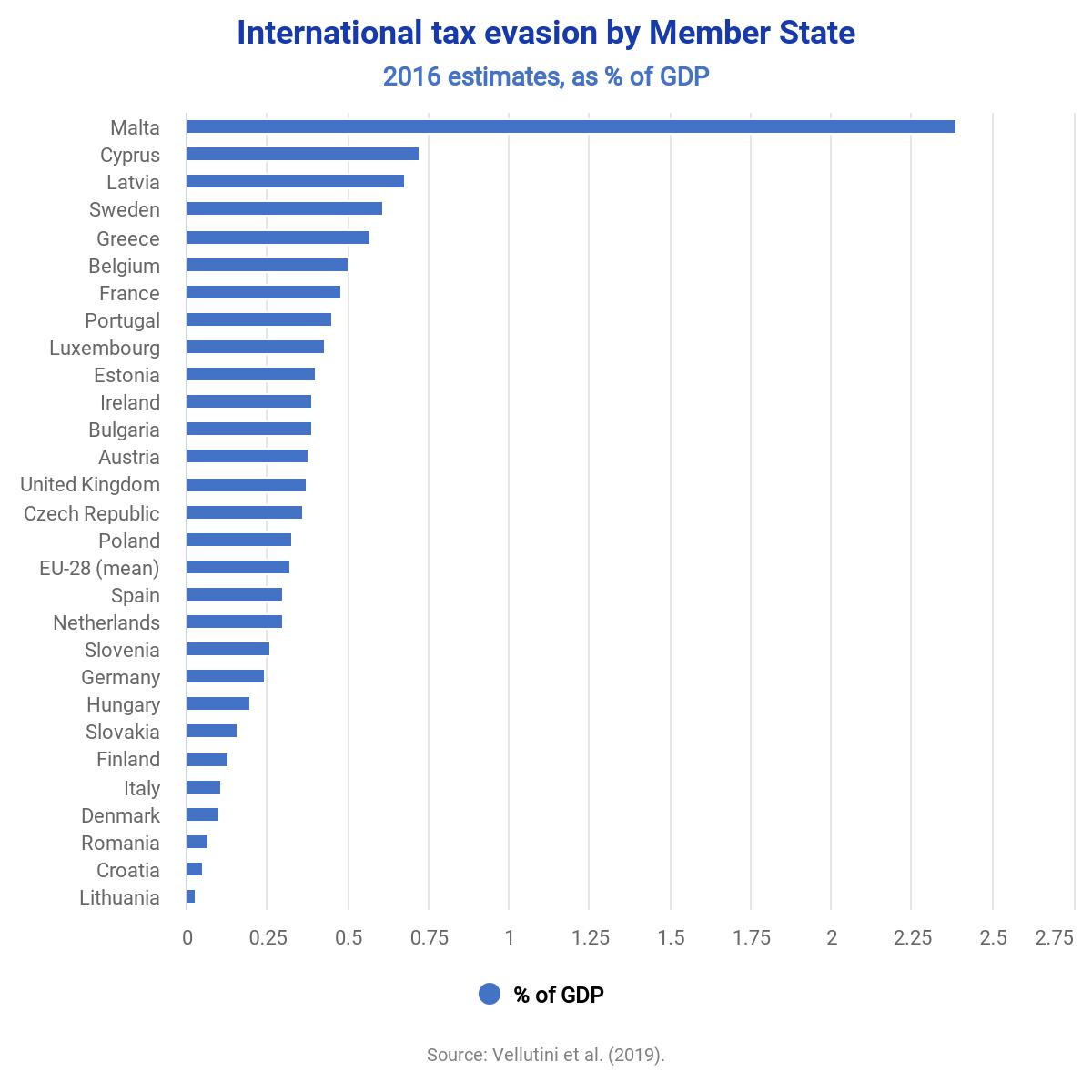

Estimating International Tax Evasion by Individuals

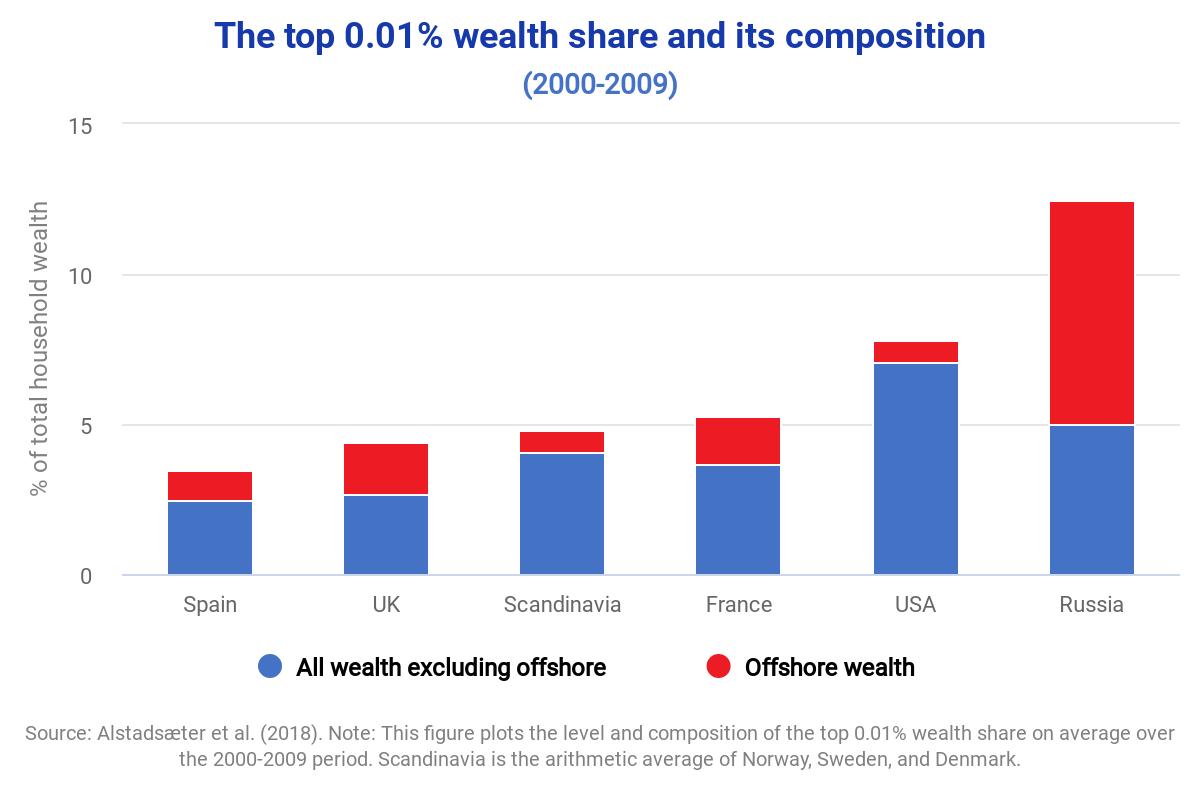

Who Owns the Wealth in Tax Havens? Macro Evidence and Implications for Global Inequality

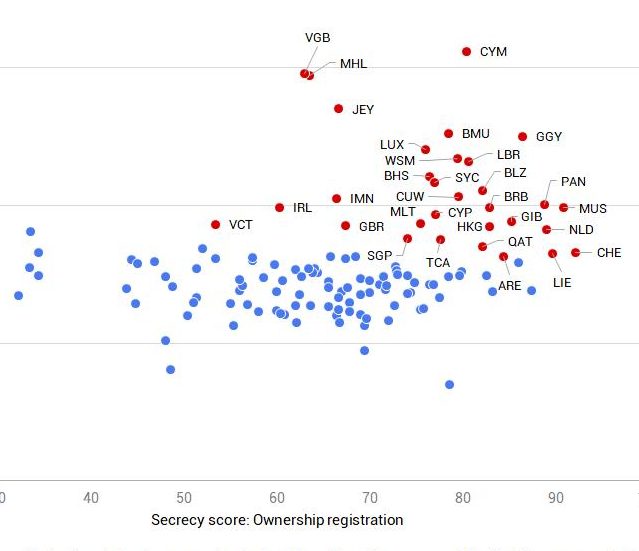

The state of tax justice 2021