Tax Evasion and Inequality

Research by Alstadsæter, Johannesen & Zucman 2019

Summary

The authors analyse inconsistencies in international macroeconomic statistics that point at the presence of undeclared capital held in offshore financial centres. These inconsistencies can be found in the International Investment Positions (IIPs) and the Balance of Payments (BP) statistics.

The BP statistics include the outflows and inflows of capital from and to the reporting country. Findings show that the cumulated capital flows do not match the stocks of assets and liabilities as reported in the country’s net international investment position. In addition, the current account balances and financial account balances in the BP do not sum up to zero across all countries which contradicts macroeconomic accounting principles. The discovered discrepancies seem systematic and consistent with the existence of undeclared assets. Thus, the authors suggest that countries tend to underestimate the holdings of foreign assets of their residents because they are concealed from the domestic authorities, for example, by holding them through custody bank accounts in offshore financial centres.

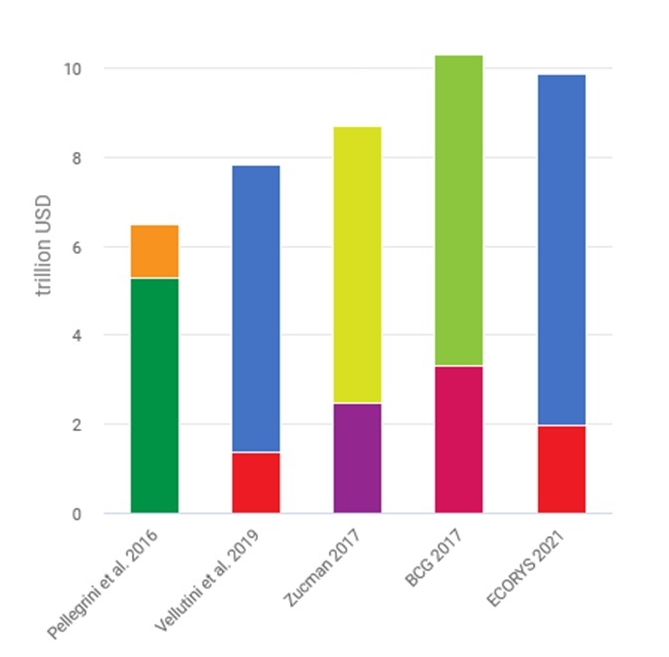

Based on these observations, Pellegrini et al. estimate that the global scale of unreported external financial assets amounts to USD 6-7 trillion in 2013 including portfolio assets and cross-border bank deposits. The ownership of unreported portfolio assets is attributed to investor countries based on the shares of reported assets that they officially own in each country. For example, if Italy owns 5% of equity issued in Luxembourg, it would be allocated 5% of the asset-liability discrepancy arising there. The global annual amount of capital income tax evasion related to these undeclared assets was estimated to range between USD 1.7 and 3.6 billion at the end of 2013. Including personal income tax evasion on the original income transferred offshore to form the hidden wealth, would yield much higher estimates of total tax revenue losses between USD 2.1 and 2.8 trillion.

Key results

Policy recommendations

Data

For their estimates of the amount of undeclared portfolio securities being held in OFCs, the authors rely on International Investment Position (IIP) statistics of the IMF and on the associated Coordinated Portfolio Investment Survey (CPIS) data [read more about the data]. Pellegrini et al. complement them with the 2015 release of the External Wealth of Nations II (EWN II), a database developed by Lane and Milesi-Ferretti. The amount of undeclared bank deposits is estimated based on the Locational Banking Statistics of the Bank for International Settlements [read more about the data].

Methodology

In this study, the authors develop descriptive data analyses and complement their base case estimates with a variety of robustness checks or sensitivity analyses.

Go to the original article

The original article was published by the Banca d’Italia. It can be downloaded from the website of the Italian central bank. [pdf]

Tax Evasion and Inequality

Tax evasion and Swiss bank deposits

Estimating International Tax Evasion by Individuals

The scale of tax evasion by individuals