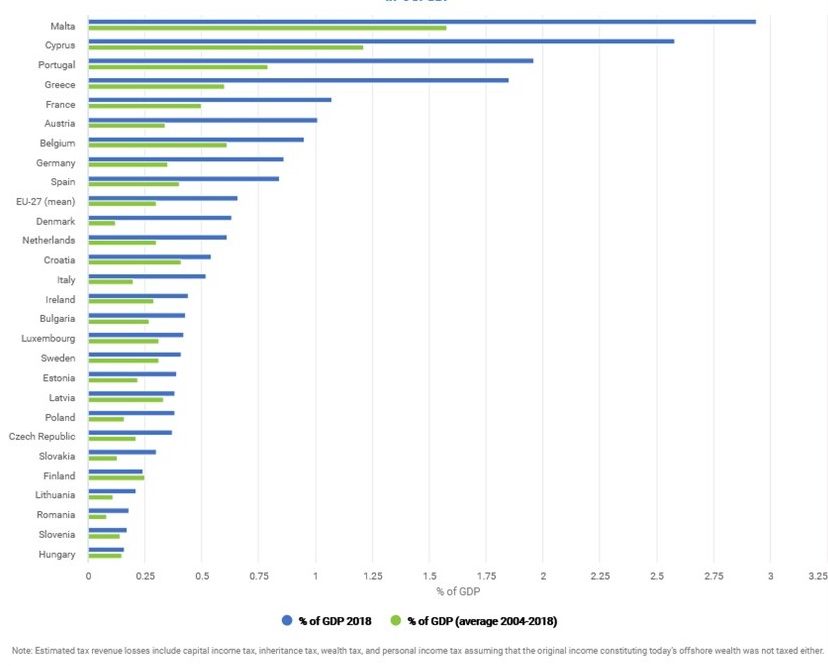

Monitoring the amount of wealth hidden by individuals in international financial centres

Report by ECORYS 2021

Bank deposits in offshore financial centres may be used to evade taxes on interest income. The EU Savings Directive adopted in 2005 limits the scope for this type of tax evasion by introducing a withholding tax of 15% on undeclared interest income earned by EU households in Switzerland and several other offshore centres. This paper estimates the impact of the withholding tax on Swiss bank deposits held by EU residents while using non-EU residents who were not subject to the tax as a comparison group. The author presents evidence that Swiss bank deposits owned by EU residents declined by 30-40% relative to other Swiss bank deposits in two quarters immediately before and after the tax was introduced. He finds similar but slightly weaker effects for other cooperating offshore centers; Luxembourg, Jersey, Guernsey, and the Isle of Man.

As the EU-owned bank deposits in Panama and Macao increased considerably in the same period, the author suggests that households with undeclared deposits transferred their funds to bank accounts in other offshore centres in which the Savings Directive did not apply. He further finds that Swiss deposits recorded as belonging to Panama increased significantly as a result of the Savings Directive which indicates that households transferred formal ownership of bank accounts to offshore holding companies in order to circumvent the reform. The decline in Swiss deposits held by countries with tax rates on interest income below 15% was not more pronounced than for countries with tax rates above 15%. This leads the author to conclude that the repatriation of funds played a minor role in explaining the estimated reduction in EU-owned Swiss deposits.

Key results

Data

Quarterly bilateral data on cross-border bank deposits held by the non-bank sector from the Bank for International Settlements

Methodology

Difference-in-difference estimation comparing the change in bank deposits with EU owners (treatment group) to the change in bank deposits with non-EU owners (control group)

Go to the original article

This article was published in the Journal of Public Economics 111 (2014). The published version of the article can be found on the journal’s website.

A working paper version can be downloaded from the Econstor website. [pdf]

Monitoring the amount of wealth hidden by individuals in international financial centres

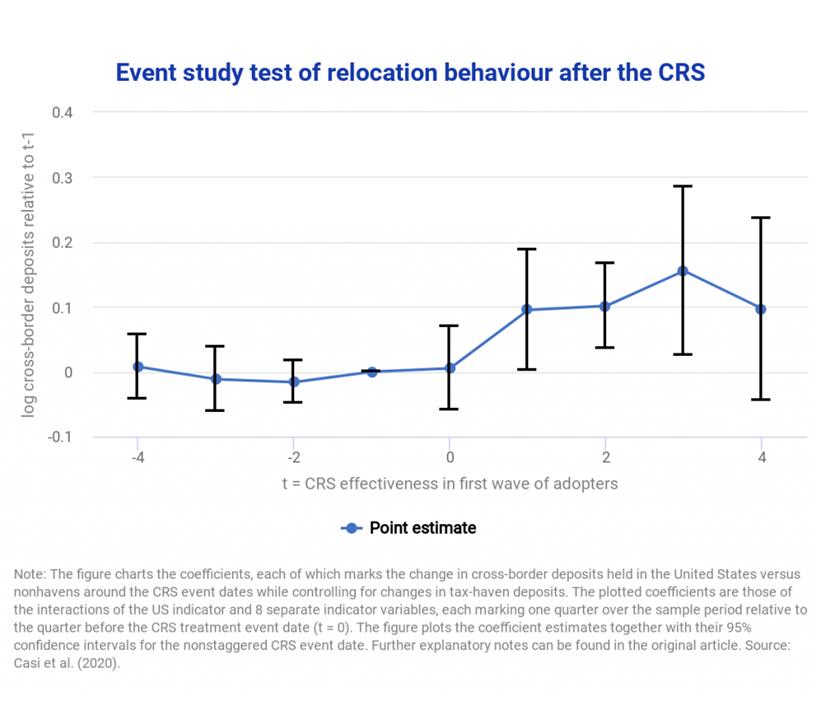

Cross-border tax evasion after the Common Reporting Standard: Game over?

Transparency and Tax Evasion: Evidence from the Foreign Account Tax Compliance Act (FATCA)

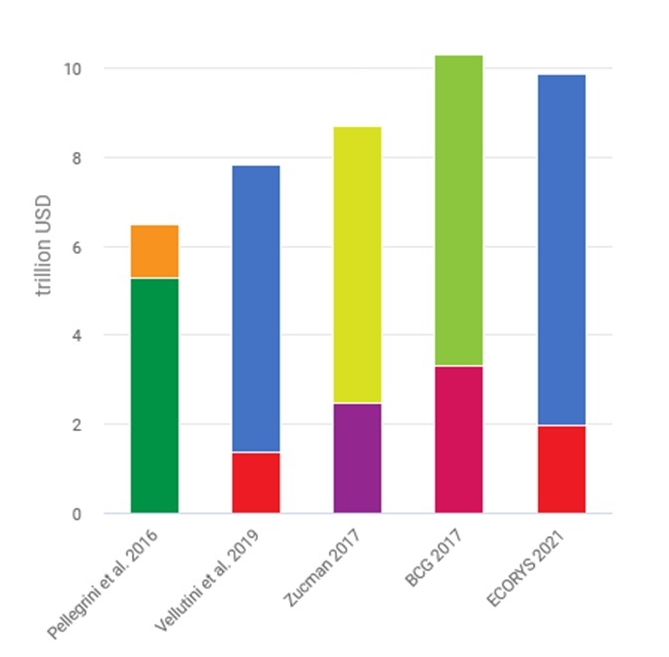

The scale of tax evasion by individuals