Hidden in plain sight: Offshore ownership of Norwegian real estate

Research by Alstadsæter and Økland 2022

Real estate prices around the world have been volatile over the past few decades, at least partly due to foreign capital. During periods of significant stress in the markets, investors tend to direct capital toward assets that they perceive as safe—also known as “flights to safe havens” (such as sovereign debt). The question that Badarinza and Ramadorai address in this paper is whether foreign real estate can also be seen as a “safe haven.” They analyze whether foreign capital is responsible for residential real estate price movements (real estate prices and price volatility) in London, especially during crises.

The authors construct a proxy for foreign investment based on two ideas: first, foreign investors are more likely to invest in the UK property market when their home countries face negative economic conditions; and second, foreign investors exhibit “home bias abroad” (i.e., they tend to choose areas in the UK where people from their home country reside).

The authors find that in areas of London with high shares of people originating from a particular country, house prices rise by an average of 1.41% and housing transaction volumes by 1.84% two years after an episode of elevated risk in that country. In terms of overall magnitudes, foreign demand accounts for 7.9% of the total variation in London house prices over the sample period. Thus, the authors find economically large, statistically significant, and robust effects of foreign risk on house prices in parts of London. The consequences are long-lasting and associated with both safe-haven effects and immigration.

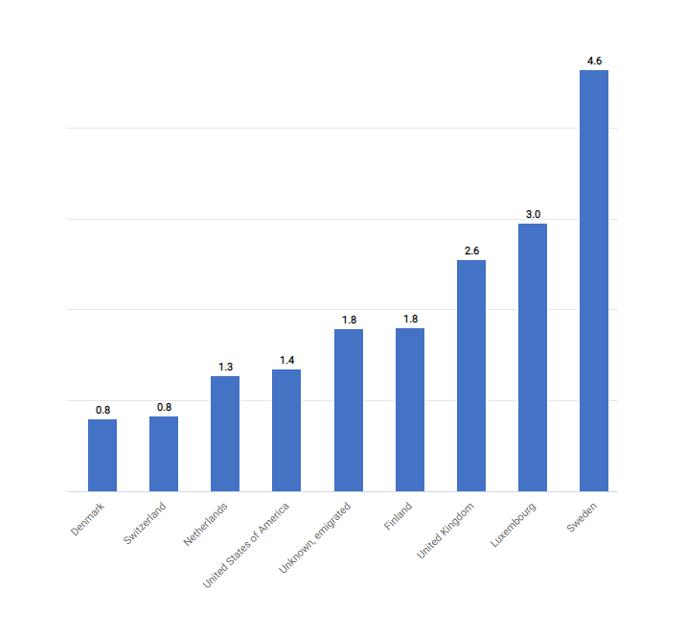

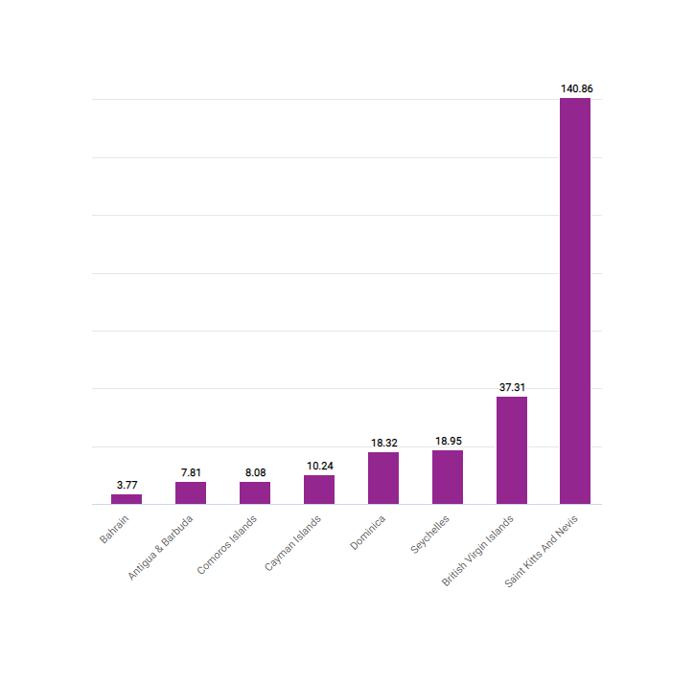

The data used reveals important knowledge gaps: most purchases by foreign-owned entities are directed through offshore vehicles, which masks the ultimate source country of the capital. The authors, furthermore, point out that purchasing real estate through a corporate entity is a popular tax avoidance device. In London, at least 85% of real estate purchases by corporate entities are routed through offshore special-purpose vehicles registered in regions such as the British Virgin Islands, Gibraltar, Cyprus, and Panama, meaning that the ultimate source of the capital is essentially untraceable.

Key results

Data

The authors use several data sets of housing transactions: two micro-level databases of housing transactions in the UK from the UK Land Registry and Nationwide Building Society; a database of cross-border commercial property transactions; and a property-level data set of ownership records. In addition, they utilize census data from the Office for National Statistics (ONS) in the UK to identify the country of origin of London residents, National Insurance registrations in London, and immigration statistics. They also use time-series indexes of country-level economic and political risk measures from the PRS Group (International Country Risk Guide) and the Polity IV Project.

The data covers the complete set of house purchases carried out through corporate entities in London from HM Land Registry. All purchasers of houses are required to report their transactions to the UK Land Registry; the data covers 2,440,618 transactions between 1995 and 2013. This constitutes 13% of the roughly 19 million residential property sales the UK Land Registry has logged for the whole of England and Wales.

Methodology

Badarinza and Ramadorai compare the evolution of house prices in London relative to the remainder of the UK and explore how this pattern relates to variations in foreign risk. To test the influence of effects such as political risks or foreign demand, they apply several panel-data fixed effects regressions.

Go to the original article

This article was published in the Journal of Financial Economics, Volume 130, Issue 3, December 2018, pp. 532–555. Go to the journal’s website.

Hidden in plain sight: Offshore ownership of Norwegian real estate

Who owns offshore real estate? Evidence from Dubai cross-border real estate investments

Homes incorporated: Offshore ownership of real estate in the U.K.

The role of anonymous property owners in the German real estate market: First results of a systematic data analysis