The state of tax justice 2021

Report by the Global Alliance for Tax Justice, Public Services International, and the Tax Justice Network

Summary

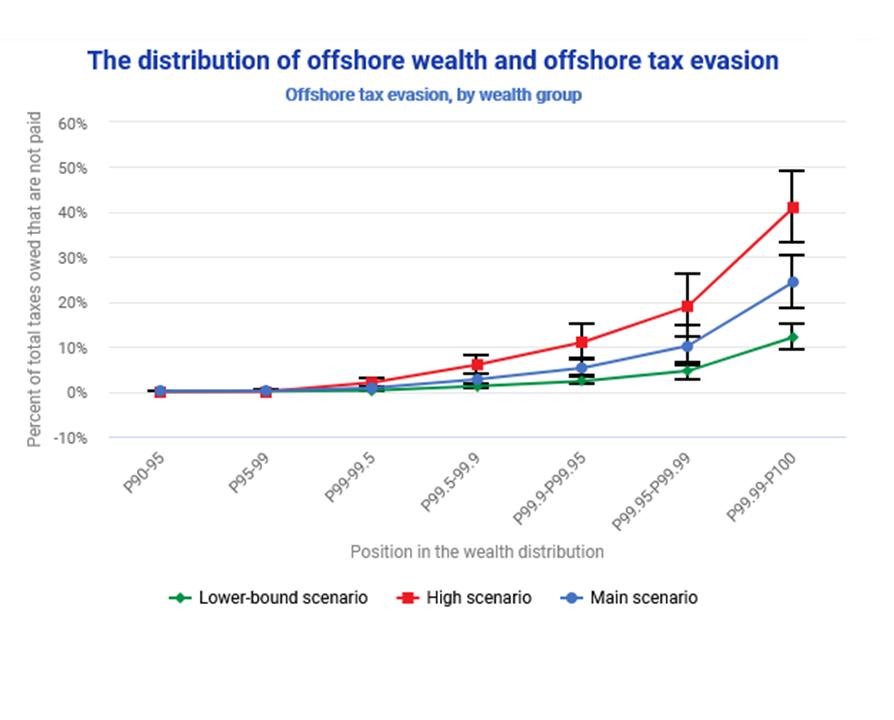

Traditional estimates of wealth inequality might underestimate wealth inequality as they ignore offshore wealth not observed in survey or administrative data. Exploiting unique datasets covering over 28,000 tax evaders in the Netherlands, the authors investigate the distribution of tax evasion and its implications for the measurement of wealth inequality. They find that the correction for offshore wealth has only a modest effect on top wealth shares in the Netherlands, which contrasts with results for Scandinavia by Alstadsæter, Johannesen and Zucman (2019). Possible explanations for the modest correction of top wealth shares might be that the wealthiest tax evaders feel less threatened by recent compliance actions as they employ more sophisticated evasion strategies. Furthermore, those wealthy households might not face sufficient incentives to evade taxes because of relatively low effective taxation at the top of the wealth distribution.

The authors further show that the distributional pattern of tax evasion depends on the offshore country of choice. The top 1% of the wealth distribution hold a majority of wealth declared through the amnesty in Switzerland and Luxembourg but not of the wealth declared in Belgium. Studying the dynamic compliance behaviour of tax amnesty participants, the authors document large and sustained increases in reported wealth of around 60% following amnesty participation. Combined with evidence of only a modest increase in the adoption of tax avoidance strategies, this suggests that amnesty participation can lead to substantial public revenue gains.

Key results

Data

The authors use administrative data on participants to the Dutch tax amnesty between 2002 and 2018; data on households which appeared in information requests to 4 different Swiss banks; administrative data on income, wealth, and demographics covering the Dutch population.

Method

The authors link the amnesty data to information on households’ income and wealth. They impute the total hidden wealth based on the self-declared wealth in the amnesty program and based on taxes ultimately recovered by the tax administration.

Go to the original article

The working paper can be downloaded from the website of EconPol Europe. [pdf]

The state of tax justice 2021

Monitoring the amount of wealth hidden by individuals in international financial centres

Tax Evasion and Inequality

The scale of tax evasion by individuals