The scale of corporate tax avoidance

How big is profit shifting? How much tax revenue is lost globally and in your country?

Summary

Bratta, Santomartino, and Acciari estimate the scale of global profit shifting and the associated corporate income tax (CIT) revenue losses. Their estimation is based on confidential Country-by-Country Reports (CbCRs) for 2017, by all multinational enterprises (MNEs) headquartered in Italy or having at least one subsidiary in Italy.

They use statutory and effective tax rates to test whether the allocation of profits by MNEs depends on the level of CIT rates in each country or on the differences of CIT rates in between countries. If MNEs report significantly more profits in low-tax countries than in high-tax countries and if this cannot be explained by economic activity or other control variables, it might indicate that they shift profits to low-tax countries to reduce their global tax payments.

The authors find that the effect of the CIT rate differential on the location of profit is particularly significant. Consistently with previous studies, they also find strong evidence of a non-linear relationship, which implies that most of MNEs’ profit shifting seems to be directed towards countries with very low tax rates while tax rate differentials between countries with average and high tax rates seem to play a minor role for profit shifting.

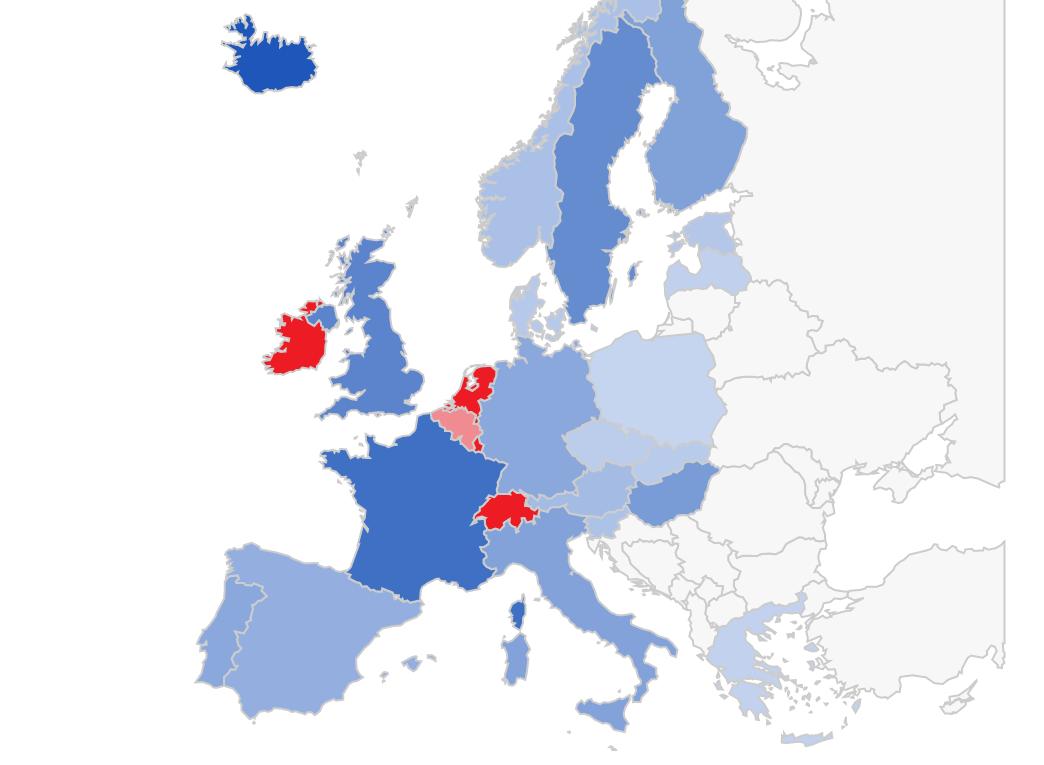

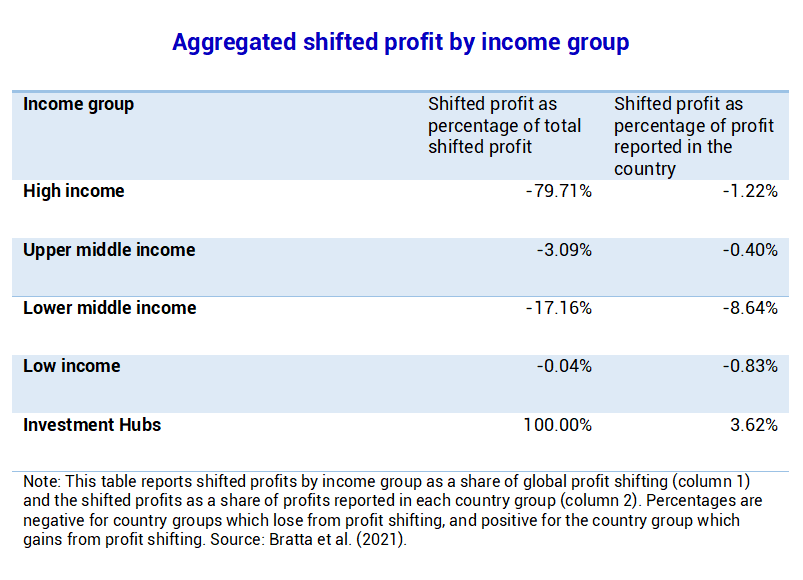

Extrapolating from their sample to the total global population of MNEs, the authors estimate that, in 2017, a total of € 887 billion of profits was shifted due to differences in tax rates which resulted in a global revenue loss of € 245 billion – a finding broadly in line with previous results. A per-country disaggregation suggests that investment hubs are the main destination of shifted profits, and high-income countries lose most in absolute terms while lower middle-income countries lose most in relative terms.

Key results

Data

The study relies on Country-by-Country Reports (CbCRs) for 2017, compiled worldwide by all MNEs having either their ultimate parent entity or at least a subsidiary in Italy. Statutory tax rates are collected from various sources: OECD corporate tax statistics dataset, the KMPG CIT rates table, as well as some national sources. The forward-looking effective tax rates are based on OECD data and data from the Oxford University Centre for Business Taxation.

Methodology

The authors exploit cross-country variation to estimate the semi-elasticity of profits with respect to tax using three possible operationalizations of the tax rate variable:

Control variables include tangible assets, the number of employees, unrelated party revenues, sector dummies and other company-level and country-level variables and multinational group fixed effects. As previous studies have found that an increase in tax rate has a much larger negative effect on reported profits in countries with substantially lower tax rates, they estimate linear and non-linear (quadratic and cubic) models. Based on the obtained semi-elasticity, they compute the global amount of shifted profits and calculate the revenue effect associated with profit shifting.

Go to the original article

The working paper was published by the Italian Ministry of Economy and Finance in 2021.

It can be downloaded from the Ministry’s website. [PDF]

The scale of corporate tax avoidance

Corporate profit shifting and the role of tax havens: Evidence from German country-by-country reporting data

How large is corporate tax base erosion and profit shifting? A general equilibrium approach

Estimating the Scale of Profit Shifting and Tax Revenue Losses Related to Foreign Direct Investment