Homes incorporated: Offshore ownership of real estate in the U.K.

Research by Johannesen, Miethe & Weishaar 2022

The authors estimate the full extent of foreign-owned commercial and residential real estate in Norway for the period of 2011–2017, including both direct and indirect ownership. Overall, 2% of Norwegian real estate assets were owned by foreigners in 2017. This share amounts to 10% for properties held by non-listed corporations, of which about 30% were owned through tax havens.

Alstadsæter and Økland uncover two underlying trends: First, foreigners own an increasing share of the Norwegian real estate through non-listed corporations. Second, the share owned through tax havens is growing even more rapidly, with Luxembourg accounting for more than half of tax haven ownership.

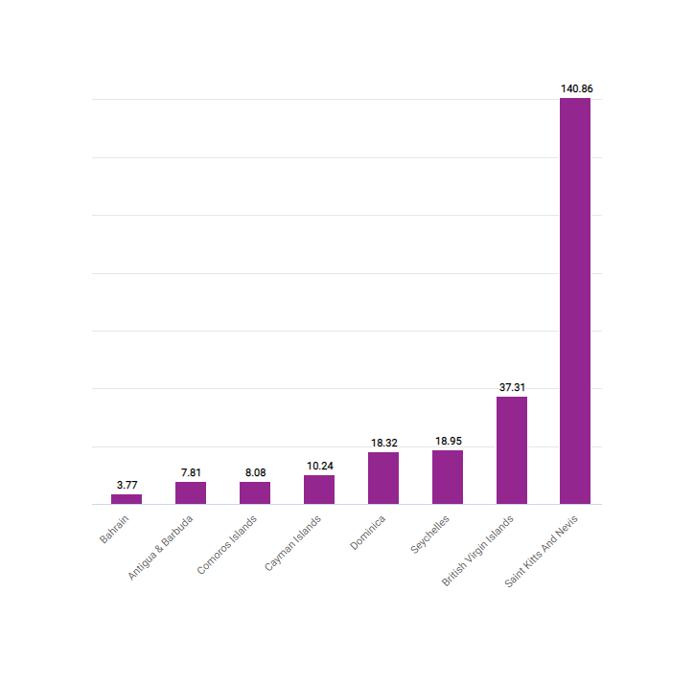

When ranking foreign ownership real estate wealth by nominal values, half of the top 18 jurisdictions are well-known tax havens. The ownership through tax havens becomes even more apparent when the real estate ownership is scaled by the GDP of the owners’ home countries. Based on this measure, the British Virgin Islands is the top jurisdiction, with ownership equal to more than 25% of its GDP. The four jurisdictions of Bermuda, Guernsey, Jersey, and Luxembourg are next, all with ownership equivalent to between 4–5% of GDP.

Key results

Data

The authors employ Norwegian administrative data covering all Norwegian properties for the period of 2011–2017. Due to Norway’s wealth tax (and the resultant tax returns), it is possible to track the general wealth of the population, including real estate assets. The estimated market values of real estate are calculated by the tax administration, which utilizes standardized and objective valuation methods.

The key limitation of the data is that it is not possible to follow the ownership chains after the immediate foreign owner. The foreign companies that own Norwegian real estate may as well be owned by residents of other countries, including Norway. This means that the analysis is not necessarily able to demonstrate the real country distribution of the ultimate owners. Instead, it shows the country distribution of ownership that is visible to Norwegian authorities and to the general public.

Methodology

Residents and corporations have unique identifiers within Norwegian administrative data, making it possible to follow individuals and non-listed corporations over time and across datasets. The corporations and individuals were merged through the shareholder register, which contains information on all Norwegian and foreign shareholders of Norwegian companies, including the exact ownership share at year-end status.

The full coverage of shareholders in Norwegian companies makes it possible to map ownership and observe the group structures and chains of holding and shell companies, in a bid to assign the ownership to the ultimate owners of companies (or in the case of foreign owners, the immediate foreign owner).

Go to the original article

The working paper can be downloaded from the EU Tax Observatory website. [PDF]

Homes incorporated: Offshore ownership of real estate in the U.K.

The role of anonymous property owners in the German real estate market: First results of a systematic data analysis

Who owns offshore real estate? Evidence from Dubai cross-border real estate investments

“We’ll always have Paris”: Out-of-country buyers in the housing market