Tax evasion and Swiss bank deposits

Research by Johannesen 2014

Summary

Beer et al. rely on restricted data on cross-border bank deposits of the Bank for International Settlements (BIS) to assess the effectiveness of different exchange of information (EOI) frameworks in tackling tax evasion. Should an EOI program be perceived as a substantial threat by tax evaders, they would be expected to reduce their foreign deposits in tax havens that signed the agreement either by repatriating funds or by relocating them to other jurisdictions not covered by the EOI.

The authors argue, that in addition to the deterrence effect on tax evaders, the EOI could also have a positive impact on deposits in cooperating tax havens because they improve tax certainty for foreign legal investors. To disentangle negative effects associated with tax evasion from positive ones, they first estimate the impact of the EOI program on deposits in offshore and non-offshore jurisdictions and then, use the difference between the two effects as an estimate for the impact of EOI on tax evasion.

Results suggest bilateral agreements on EOI on request have insignificant or relatively low negative effect on deposits held in offshore jurisdictions. Automatic EOI programs, in contrast, seem to have a relatively strong negative effect of 25%. The authors provide further evidence on the superiority of AEOI by analysing the effects of all existing bilateral EOI agreements over the past 20 years. Lastly, they find evidence that EOI programs curb “round-tripping” schemes, i.e. investment by a non-offshore resident in her home country through a tax-haven shell company.

Key results

Policy implications

Data

Based on the restricted locational banking statistics of the Bank for International Settlements (BIS), Beer et al. analyse foreign deposits in 39 reporting jurisdictions by deposit holders from more than 200 jurisdictions. The time period considered spans from Q1 1995 to Q2 2018. 17 of the reporting countries are classified as offshore jurisdictions according to Johannesen and Zucman (2014).

The information regarding EOI agreements is drawn from various sources. EOIR programs are covered by the OECD’s Exchange of Tax Information Portal. Information about the Savings Directive is collected directly from the website of the European Commission and that about FATCA comes from the US Treasury’s website. Eventually, the 4,600 country pairs covered by the CRS at the time of publication are taken from the OECD’s Automatic Exchange Portal.

Control variables (GDP and foreign exchange rates) are collected from the IMF’s World Economic Outlook database and from the World Bank’s Governance indicators. A variety of complementary data sources are used to estimate the final finite mixture model.

Methodology

Beer et al. introduce a triple-differenced estimator as a new methodology to isolate the effect of EOI programs on tax evasion. To test the sensitivity of their estimates to the list of offshore jurisdictions, they employ a data-driven stochastic classification procedure. With the help of a finite mixture model, they simultaneously obtain both a probabilistic classification of countries as offshore centres and an estimation of the response of foreign deposits to information exchange.

Go to the original article

The original working paper can be downloaded from the website of the IMF.

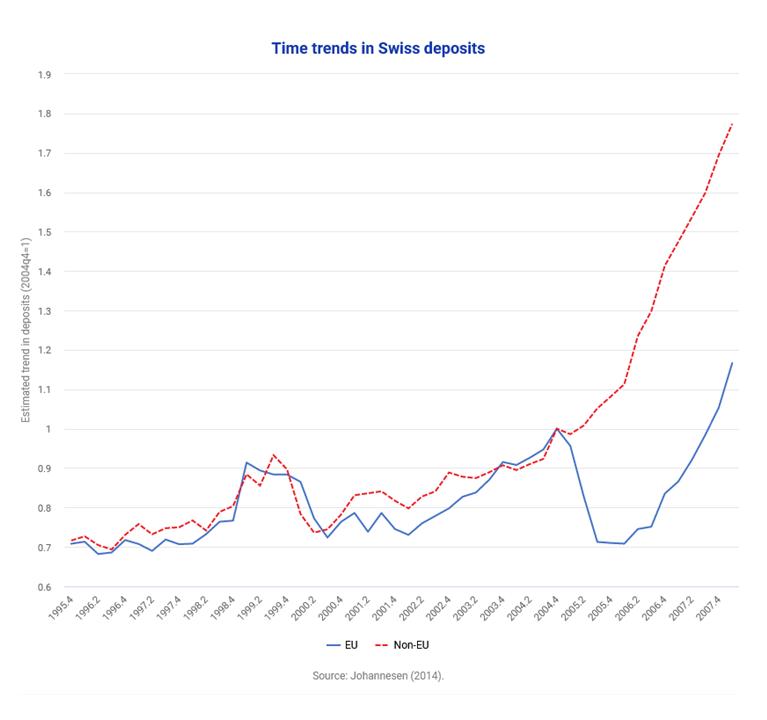

Tax evasion and Swiss bank deposits

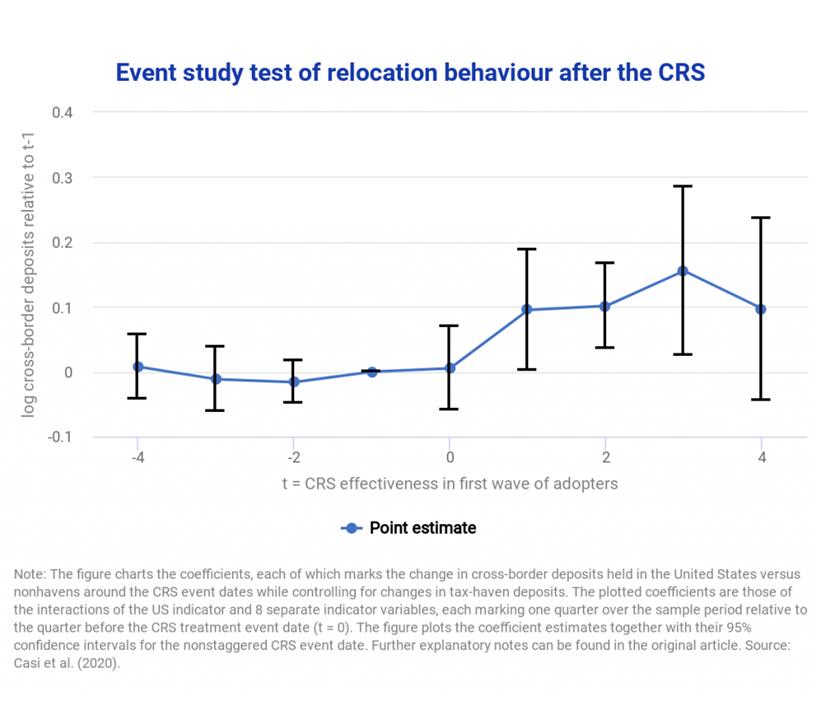

Cross-border tax evasion after the Common Reporting Standard: Game over?

Bank Secrecy in Offshore Centres and Capital Flows: Does Blacklisting Matter?

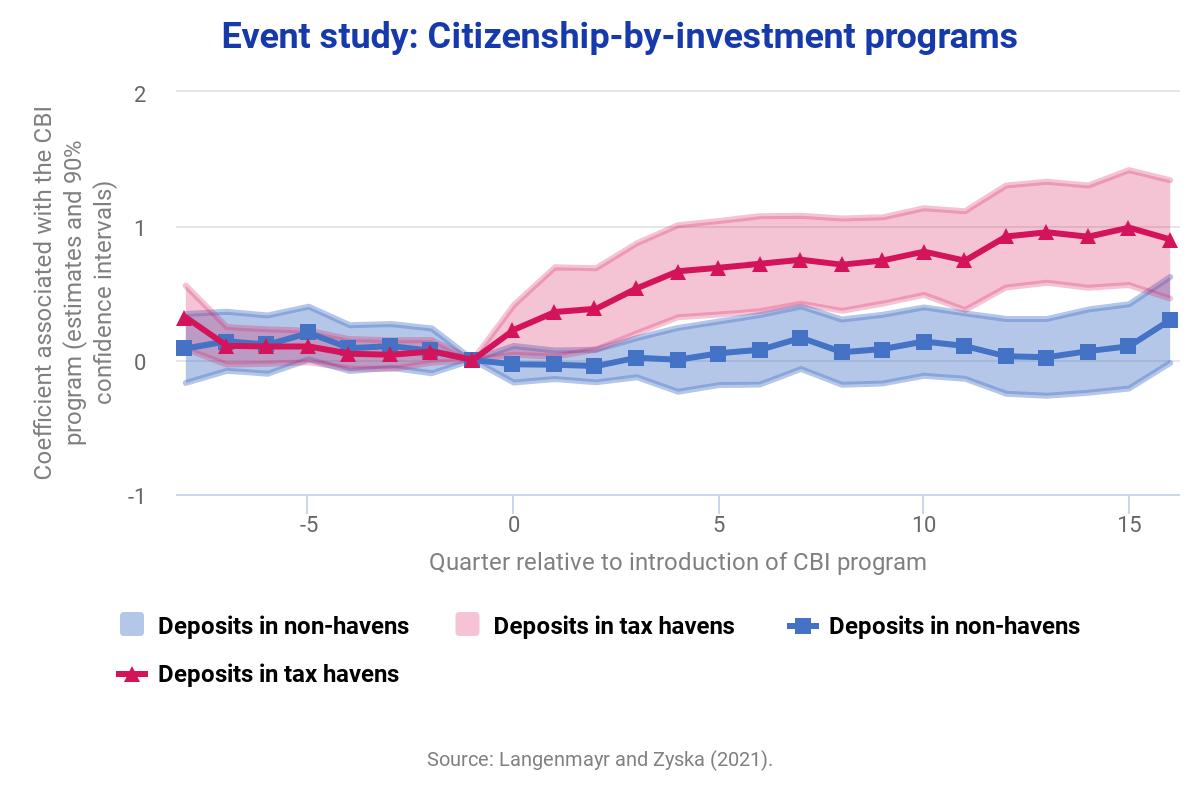

Escaping the Exchange of Information: Tax Evasion via Citizenship-by-Investment