Hidden in plain sight: Offshore ownership of Norwegian real estate

Research by Alstadsæter and Økland 2022

Real estate markets are highly vulnerable to inflows of illicit financial flows, as real estate ownership in or through tax havens creates opportunities for tax evasion and money laundering. Investment through shell companies which conceal the beneficial owner of real estate properties may have undesirable effects in housing markets or can be used to evade international sanctions.

Real estate has been a blind spot in statistics on international investments for years. Information on tangible assets owned by households outside their country of residency is limited and data is often neither centralized nor accessible for research. As a result, little is known about who owns real estate in tax havens, who owns real estate through shell companies located in tax havens and how much of this wealth has been duly reported to domestic authorities.

Furthermore, since the automatic multilateral exchange of information between tax authorities enforced in 2017 does not cover tangible assets, there is an incentive to convert financial assets into real estate to preserve anonymity. Recognizing the importance of this issue, this page provides an overview of the current state of research on cross-border ownership of real estate and the role of tax havens.

Alstadtsæter, Økland, Planterose & Zucman (2022): Who owns offshore real estate? Evidence from Dubai.

The authors analyse a micro-dataset capturing the private and corporate ownership of about 800,000 properties in Dubai. They find that:

Morel & Uri (2021): The increase in real estate investments made by non-residents is driven by expatriates.

The authors analyse the development of direct investment in French residential properties by non-residents. They find that:

> read more about this research

Cvijanovic & Spaenjers (2020): “We’ll always have Paris”: Out-of-country buyers in the housing market.

The authors analyze real estate transaction data to explore the influence of non-resident foreigners in the Paris housing market. They find that:

> read more about this research

Miethe, Peichl & Trautvetter (2022): Die Rolle von anonymen Immobilieneigentümern am deutschen Immobilienmarkt: Erste Ergebnisse einer systematischen Datenauswertung.

The authors gather data on real estate owned by corporate entities from five German states and cities and investigate the country of ultimate beneficial owners. They find that:

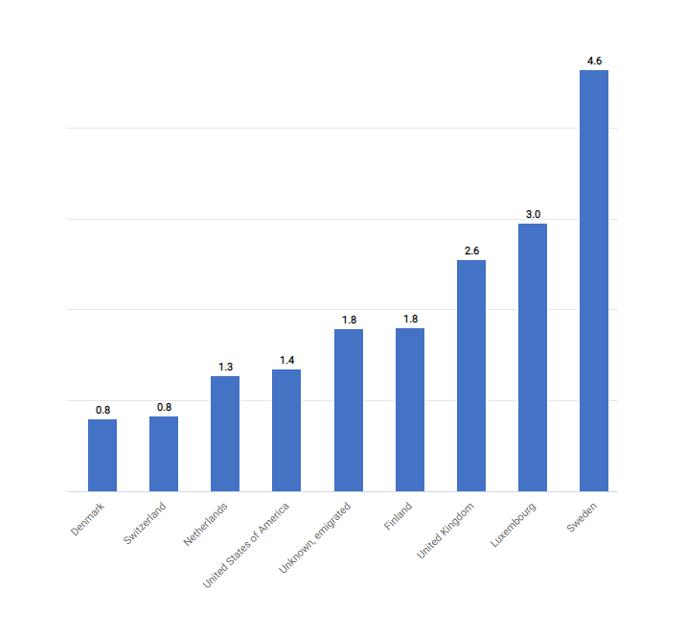

Alstadtsæter & Økland (2022): Hidden in plain sight: Offshore ownership of Norwegian real estate.

The authors analyze Norwegian administrative data to map foreign owned commercial and residential real estate and its links to tax havens. They find that:

Agarwal, Chia & Sing (2020): Straw purchase or safe haven? The hidden perils of illicit wealth in property markets.

The authors explore real estate transaction data and offshore leak data from the Panama Papers to analyze how individuals associated to the Panama Papers behave in housing transactions occurring in Singapore. They find that:

Johannesen, Miethe & Weishaar (2022): Homes incorporated: Offshore ownership of real estate in the UK.

The authors analyze several micro-data sources, from administrative data to offshore data leaks, to reveal the ultimate beneficial owners of real estate in the UK. They find that:

> read more about this research

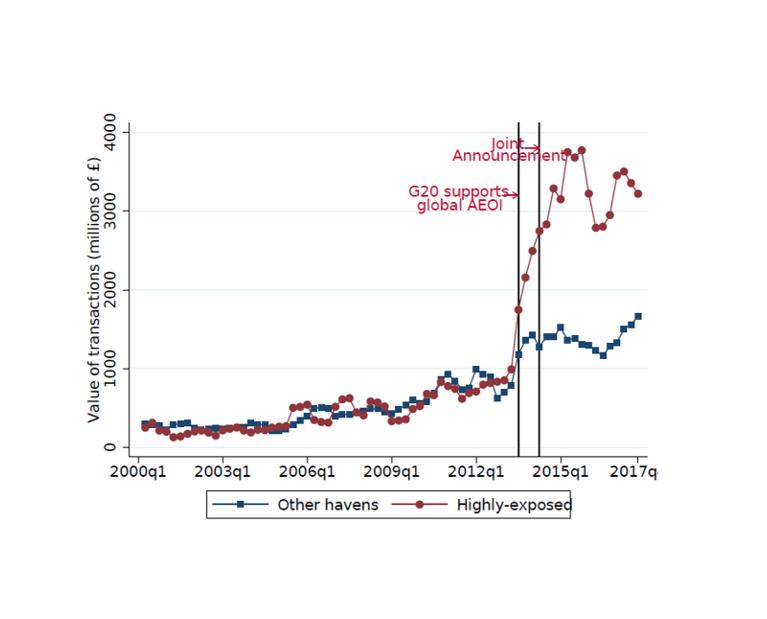

Bomare & Le Guern Herry (2022): Will we ever be able to track offshore wealth? Evidence from the offshore real estate market in the UK.

The authors analyze administrative data on real estate purchases made by foreign companies in the UK and leaked data to trace ultimate ownership for a subsample of transactions. They find that:

> read more about this research

Badarinza & Ramadorai (2018): Home away from home? Foreign demand and London house prices.

The authors analyze several data sets of housing transactions and country-level economic and political risk measures to explore the influence of foreign risk on London house prices. They find that:

> read more about this research

Sá (2016): The effect of foreign investors on local housing markets: Evidence from the UK.

The author analyses administrative data to explore the effect of foreign investment by overseas companies on the housing market in England and Wales. She finds that:

Collin, Hollenbach & Szakonyi (2022): The impact of beneficial ownership transparency on illicit purchases of U.S. property.

The authors analyze data on 39 million real estate transactions in the US over the period 2014–2019 to estimate the effect of beneficial ownership transparency on property purchases. They find that:

Hidden in plain sight: Offshore ownership of Norwegian real estate

Homes incorporated: Offshore ownership of real estate in the U.K.

Who owns offshore real estate? Evidence from Dubai cross-border real estate investments

Will we ever be able to track offshore wealth? Evidence from the offshore real estate market in the UK