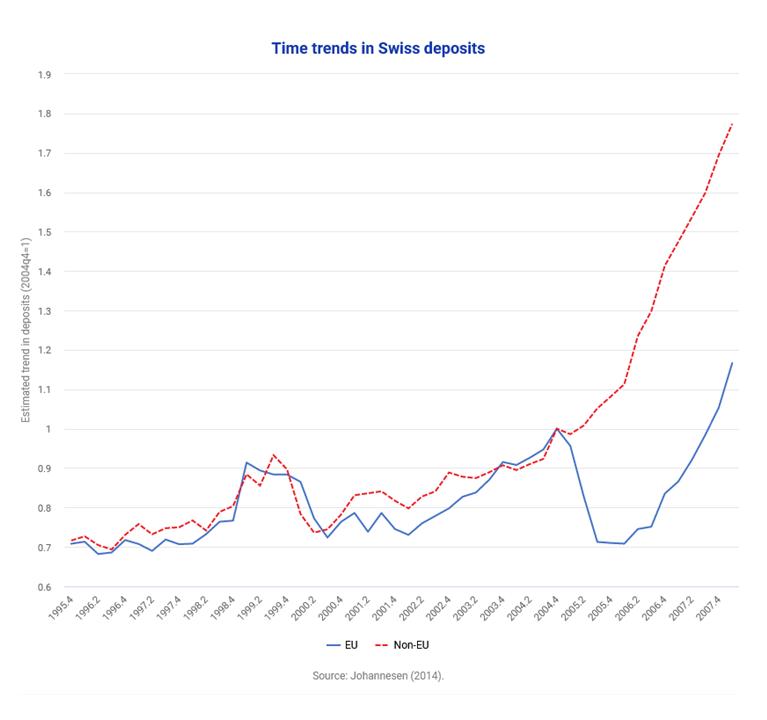

Tax evasion and Swiss bank deposits

Research by Johannesen 2014

Summary

In this article, the authors analyse the effectiveness of the Foreign Account Tax Compliance Act (FATCA), implemented by the US government in 2010 in order to tackle US individual offshore tax evasion. This regulation represented a significant shift from self-reporting to automatic and mandatory reporting by foreign financial institutions. The authors examine whether the implementation of FATCA led U.S. investors to move their financial assets out of tax havens by comparing the development of haven-sourced foreign portfolio investment (FPI) into the U.S. before and after the implementation of FATCA.

They find that equity investments from tax havens into the US declined by 21% from 2012 to 2015 which would be consistent with a decrease in “round-tripping” investment activity attributable to U.S. investors’ offshore tax evasion activities. Under the assumption that individuals have a preference for investments in their home country and that foreign investors were not affected by FATCA, the authors impute these “abnormal” changes in Foreign Portfolio Investments (FPIs) since 2012 to the impact of the regulation.

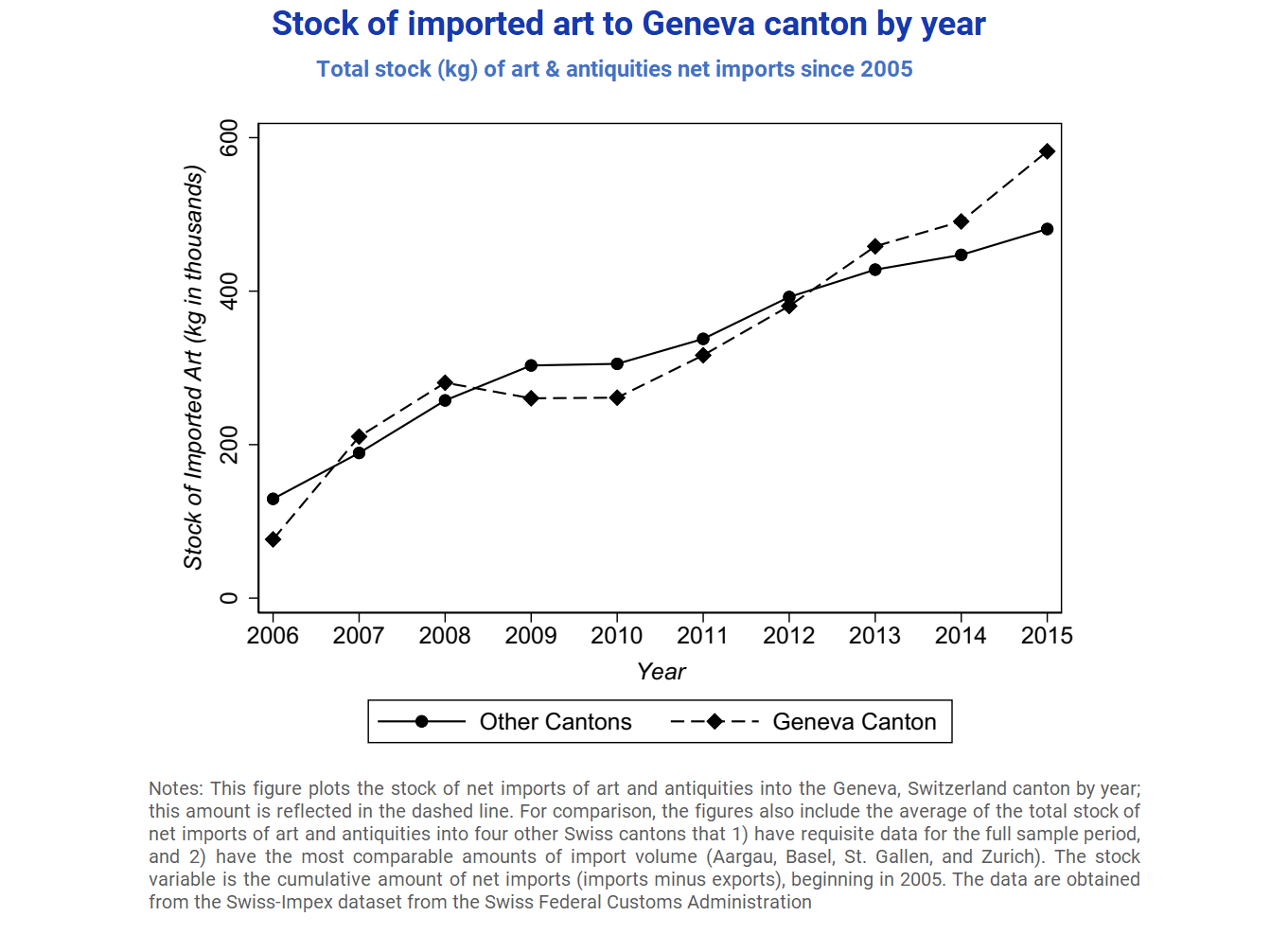

However, they find evidence of additional consequences and negative externalities of the regulation, including a surge in expatriations and increased investments in alternative asset classes not covered by FATCA reporting requirements. For instance, the authors suspect a shift from financial assets to real estate because, in the post-FATCA period, they observe a sharp increase in the house price index of countries without foreign buyer restrictions as compared to countries with such restrictions. In addition, they observe that imports of art works in Geneva – where one of the largest freeports in the world is located – increased with respect to art imports in other Swiss cantons without freeports.

Key Results

Policy Implications

Data & Methodology Used

The authors use various data sources including:

Methodology

Various regression analyses. Most regressions relate the dependent variable of interest to a post-FATCA dummy variable interacted with other dummies in order to identify diverging trends between sub-groups of variables more or less affected by FATCA.

Go to the Original Article

This article has been published in the Journal of Accounting Research 58(1) in 2019. The published version of the paper can be found at the journal’s website.

A working paper version can be downloaded from the website of the Stanford Graduate School of Business. [pdf]

Tax evasion and Swiss bank deposits

Cross-border tax evasion after the Common Reporting Standard: Game over?

Hidden treasures: The impact of Automatic Exchange of Information on cross-border tax evasion

The scale of tax evasion by individuals